Story #4 — Inflation accelerates

To the surprise of many, the US CPI rose 0.1% in August, after being unchanged in July. Prices were up 8.3% year-over-year, down from 8.5% in July, but above analysts’ expectations of 8.1%. Core inflation rose 0.6% in August, and was up 6.3% year-over-year, accelerating from 5.9%. A hotter-than-expected inflation reading strengthen the Fed’s case for more aggressive interest rate hikes (see next story). Eurozone inflation hit double digits for the first time ever, jumping to record 10% in September. Core CPI accelerates to fresh all-time-high as well. Inflation is broadening on a global scale basis as almost 90% of countries are currently facing headline inflation above 6% on a yoy basis.

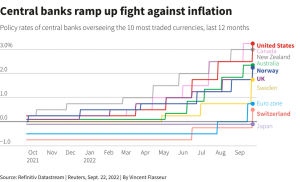

Story #5 — Central banks continue to tighten

The quarter was off to a strong start for risk assets with the S&P 500 being up by nearly +14% in total return terms over July and early-August as a result of a bear market rally. That was supported by a belief in the “peak inflation” narrative, suggesting that we had seen the worst of rapid price gains, and that the Fed would thus be able to pivot towards rate cuts moving into 2023. This narrative was supported by a dovish interpretation of the July FOMC meeting, during which Fed Chairman Jeremy Powell said that as “monetary policy tightens further, it likely will become appropriate to slow the pace of increases”. But everything shifted by mid-August in a very hawkish speech from Powell at the Jackson Hole symposium. The Fed then followed through on this hawkish rhetoric, delivering a third consecutive 75bps rate hike at their September meeting. Furthermore, the median dot indicated that officials favored a further 125bps of hikes this year at the two remaining meetings, with the Fed Funds rate still at 4.6% by end-2023.

The story was quite similar at the ECB. At the start of Q3, the ECB was expected to start its tightening cycle in July with a 25bps hike. However, with inflation continuing to rise to new records, they finally hiked by 50bps in July, and followed up with an even stronger 75bps move in September.

For financial markets, the key story of the quarter was thus the fact that central banks became more explicit about how they would be willing to keep policy in restrictive territory, even if growth was to slow. Indeed, September FOMC’s meeting showed that policymakers are willing to keep rates in restrictive territory even if that meant a noticeable rise in unemployment.

Story #6 — Mighty dollar

The only main asset class which was up in the third quarter was the US Dollar, which strengthened against every other G10 currency as the Fed reiterated its hawkishness. Over the quarter as a whole, the dollar index strengthened by +7.1%, marking its strongest quarterly performance since Q1 2015. It also marked the first time since the late-1990s that the dollar has strengthened for five consecutive quarters.

While the dollar index continues to appreciate, a detailed analysis shows a significant performance differential between two categories of countries: those in the G10 and emerging countries (excluding China and Russia). It can be seen that, contrary to other periods of crisis, emerging countries are far more resilient than developed countries.