Reflecting on history, a clear pattern emerges: leading megatrends tend to seed tomorrow’s mega-caps. The internet is the obvious example: a structural shift in the early 2000s that helped produce Amazon, Alphabet, and Meta as some of the world’s largest companies two decades on. Put simply, thematic investing is a repeatable way to target structural growth by signposting the most promising corners of the equity universe.

Yet naming a theme and owning it are two different things. Once investors decide that Artificial Intelligence (AI) or European infrastructure matter for multi-decade growth, the hard question is: what does investing in AI or investing in EU infrastructure actually mean in practice?

Our thematic investment philosophy is built around one priority: delivering thematic portfolios that are as aligned as possible to the theme.

Same theme, different stocks: the dispersion problem

One clear empirical lesson from studying thematic active funds and ETFs is that, even when they claim to provide access to the same theme, they often hold very different baskets and therefore deliver very different returns.

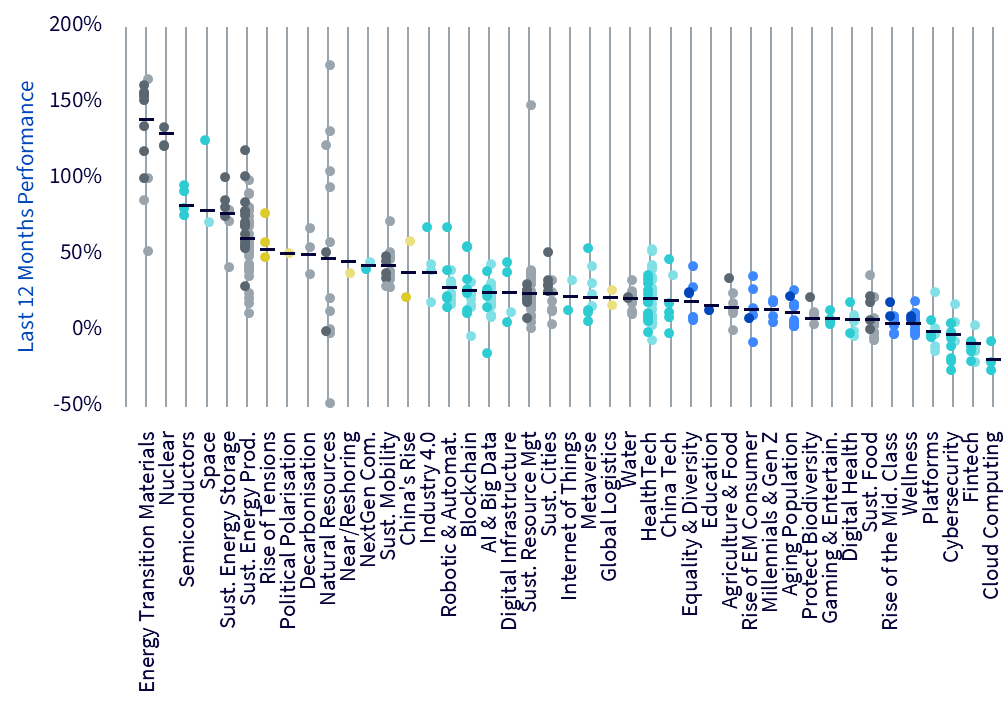

In Figure 1, we show the performance over the last 12 months for all European-domiciled thematic active mutual funds and exchange-traded funds (ETFs), organised by theme. Each column in the graph represents a theme, and each dot represents a strategy. Looking at the dispersion of the dots in each column, it is very clear that the performance of strategies in the same theme diverges a lot. Taking two examples:

Energy Transition Materials is the best performing theme for the period, with an average performance of 139% over the period. However, the best strategy returned 234% while the worst one returned 52.4%. This is a 182% performance gap for two strategies in the same theme[1].

Semiconductors is the third best theme. It is also a theme that should be pretty well defined, and yet the best strategy returned 96.1% in the last 12 months when the worst one returned 76.2%[2].

Figure 1: Last 12-month performance dispersion by theme in European domiciled thematic strategies

Source: WisdomTree, Morningstar, Bloomberg. From 28 February 2025 to 28 February 2026. Performance is calculated in US Dollars. The list of Europe-Domiciled ETFs and Open-ended mutual funds has been compiled by WisdomTree as part of the WisdomTree’s own thematic classification. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Why such divergence? Because there is no single, recognised benchmark for a theme like AI or quantum computing. When a manager invests in a US small cap, it is clear what the investment universe is and what the benchmark is. As a result, managers make very different stock-selection and weighting choices and outcomes vary accordingly.

The pitfalls to avoid

When considering which portfolio is relevant to a given theme, there are two serious mistakes to avoid:

1. Overconcentration in a few names. The late-1990s internet example shows the risk: buying the ten largest dot-com names would have beaten the market long term only because the basket happened to include Amazon; many other names failed. Because equity returns are highly asymmetric (few winners drive most of the wealth creation), being right about which companies win matters far more than avoiding the many losers. The antidote is humility: broaden the net to increase the probability of owning future winners.

2. Mistaking today’s mega-caps for thematic exposure. Mega-caps have ridden prior waves of structural change. But they cannot keep compounding at the same exponential rates indefinitely, nor should a thematic strategy be a rerun of the Nasdaq top-ten. If a thematic sleeve leans heavily on current hyperscalers, it is functionally a market or sector bet, not a true thematic exposure. Thematic portfolios must be differentiated from broad market and tech indices if they are to capture tomorrow’s growth.

When it comes to thematic investing, there is a clear case for a disciplined, research-driven approach that maximises thematic beta while controlling for concentration and benchmark overlap.

Our philosophy: alignment first, then expertise and purity

WisdomTree Thematic Investment Philosophy rests on five pillars:

- Alignment to the theme: Opportunities within each theme are captured with a tailored methodology to maximise their investment potential.

- Expertise: We collaborate with external industry experts where beneficial while leveraging WisdomTree’s in-house research and product development capabilities.

- Purity: Companies are selected based on their strong alignment with the theme offering pure-play exposure and growth potential.

- Differentiation: Our strategies stand out from broad benchmarks and other thematic products, offering investors true differentiation and diversification benefits.

- Discipline and Transparency: Strategies follow a clearly defined framework to ensure precision and consistency in portfolio construction.

Alignment is the lynchpin. A thematic portfolio must visibly and mechanically track the economic drivers of the theme you want to invest in. In practice, that means there is no cookie-cutter approach to a theme that can be applied successfully to every theme. In this case, one size does not fit all. Each theme requires a bespoke construction. This is why, at WisdomTree, we develop unique strategies tailored to each theme (meaning strategies differ widely from theme to theme).

Conclusion: a short checklist for investors

Thematic ETFs offer a way to point capital at structural growth potential. But execution matters. Before allocating, ask three simple questions:

- Alignment: Does the fund mechanically capture the economic exposures that define the theme?

- Purity and expertise: Is stock selection expert-driven and focused on pure players with high thematic revenue?

- Differentiation and tradability: What is the overlap with MSCI/Nasdaq, and is the implementation liquid and scalable?

If the answers are affirmative, the investment is a genuine thematic satellite, not another way to own today’s mega-caps. That distinction is what separates talk from outcome in thematic investing.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

By Pierre Debru, Head of Research, Europe, WisdomTree

[1] – Source: WisdomTree, Morningstar, Bloomberg. From 28 February 2025 to 28 February 2026. Performance is calculated in US Dollars. The list of Europe-Domiciled ETFs and Open-ended mutual funds has been compiled by WisdomTree as part of the WisdomTree’s own thematic classification.

[2] – Ibid.