What is the near-term corporate impact?

Germany’s reliance on the Nord Stream 1 pipeline, and lack of alternative options, means it is the major economy most at risk of gas shortages. Earlier this year, the German government unveiled a three-step plan for gas rationing that could see supply reduced to industry in order to ensure availability for households and critical institutions like hospitals.

Under such a scenario, energy-intensive sectors such as metals production and chemicals would be the most affected in the short term.

Arianna Fox, European Equities Analyst, said: “The chemicals industry is one that is directly exposed to gas shortage risk given how energy-intensive it is and how so much of the industry is concentrated in Germany. The government could introduce rationing but there are still many questions as to how this would play out.

“For example, would all industries face the same level of rationing? It might be the case that the government would try to protect industries such as food & beverage production, or healthcare companies. If that’s the case, then other industries like chemicals would have to shoulder a larger burden, hitting their production harder.

“The trouble is that chemicals are used in so many products and processes. Ultimately, every industry would feel the impact of reduced supply or higher prices for chemicals. Businesses could try to import the chemicals they need from outside of Europe but supply chains are still disrupted post Covid, and there’s no guarantee that plants outside Europe have spare capacity.”

Of course, rationing is not currently in place, but financial markets hate uncertainty. Share prices of European chemicals companies have fallen sharply as a result.

Arianna Fox said: “Some chemicals companies may potentially look like attractive investments, given how far shares have already fallen, especially if the ‘worst case scenario’ of a shut-off of Russian gas does not transpire.”

And indeed, it may be that the much-feared cut-off of all Russian supply does not materialise.

Mark Lacey said: “We think that a continuation of pipeline flows (albeit at reduced levels) is more likely than a complete cut-off. A cut-off would see Russia lose all its political and economic leverage over Europe. Also, the lost revenues from gas sales must be having a significant impact on the country’s export revenues.”

It may also be that households are asked to shoulder more of the burden, which would help to protect the corporate sector. Germany has unveiled plans for a levy on gas that would affect households too.

Possible recession poses another risk

The high gas prices are just one of several factors that could weigh on economic activity. German GDP growth was zero in Q2, albeit Q1 growth was revised higher.

Azad Zangana said: “We continue to expect reasonable growth for southern EU member states, which have not enjoyed a full tourism season since 2019.

“However, it’s clear from Germany’s performance that global capital investment has slowed in response to rising interest rates and concerns over growth. China’s lockdowns have not helped matters either. With the heavy reliance on Russian gas to consider as well, it appears that the northern member states are particularly vulnerable going into the next two to three quarters.”

The possibility of a broader economic slowdown, or recession, further complicates the options of companies such as the chemicals producers who may be forced to cut their production volumes due to lack of gas.

Arianna Fox said: “Typically, companies facing volume declines try to protect profits by raising prices. But that’s difficult for chemicals firms in the current environment where customers have already endured price hikes. Instead, demand may be likely to fall.”

When will prices ease?

Demand for gas is not only high in Europe, but around the world. Countries are seeking to close down polluting coal plants and move to natural gas as an interim step towards reducing their greenhouse gas emissions. This means Europe is currently competing with countries such as India and China for LNG, with cargoes going to those who can pay the highest prices.

Another problem is that there is limited new LNG supply coming to the market over the next two years.

Mark Lacey said: “The main reason for this lack of supply is due to under-investment in upstream gas projects and project deferrals. This is largely because of the Covid-19 pandemic, as well as previously low regional gas prices.

“However, beyond the next 24 months, Europe starts to have some alternative options for the supply of gas. That’s when we’ll start to see the ramp-up of new supply from the US and Qatar.”

That said, even when new LNG supply becomes available, gas prices are unlikely to come down to their previous levels given the growing demand from other regions and for gas as a transition fuel.

Mark Lacey said: “European (and Asian) gas prices have clear downside risk from current levels, but when they do ‘normalise’, they are likely to retrace to a higher base level. For example, rather than $5 – $10/mcf long term pricing, $12 – $18/Mcf pricing may be more sensible.”

This would have long-term implications for energy-intensive sectors like chemicals, even once the current crisis is over. They would still face higher costs than they had previously been used to, impacting their profitability.

Arianna Fox said: “This could cause a longer-term structural shift that would reduce the competitiveness of chemicals companies producing in Europe. Chemicals companies may seek to shift production to countries where the cost of gas is cheaper.”

Are there any winners?

In the medium to long term, a winner from the gas crisis is likely to be the renewable energy sector. The need to curb harmful emissions and to reduce reliance on Russian fossil fuel imports go hand in hand.

Renewable energy projects like wind or solar farms may not be instant solutions to the problem, but they are a lot quicker to get up and running than a nuclear power station, for example.

Higher power prices are also feeding into long-term contract prices for power, meaning investment returns on such projects now look more attractive.

Mark Lacey said: “Power purchase agreements (PPAs) have been increasing steadily from €40/Mwh in March 2021 to just under €100/Mwh in June 2022.

“This has a direct impact on renewable project returns, with developers noting that some project internal rates of return (a measure used to estimate profitability) have increased from 5-6% two years ago, to closer to 11-12% now.”

In May this year, the EU unveiled its “RePowerEU” plan which is designed to phase out dependency on Russian gas and ensure a more diversified supply of power from lower emission sources. This summer’s crisis and the low gas volumes coming from Russia heighten the need for that phase-out to accelerate. Ultimately, this will bring prices down and make the EU more self-sufficient in terms of power generation.

But it may not be a straightforward journey towards renewables. For example, measures to cushion the gas price impact on consumers may have unintended consequences.

Economist Irene Lauro said: “Governments are providing measures to shield vulnerable households from rising energy prices via subsidies, scrapping surcharges or capping electricity prices.

“Subsidising energy consumption is important to help consumers with the cost of living crisis in the short run. But it can have some drawbacks, indirectly incentivising the use of fossil fuel energy and making the required switch from dirty to cleaner technologies even more expensive in the long run.”

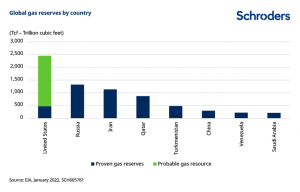

However, in the near term, there is a winner that emerges from the current crisis: US gas producers. The higher gas prices make it economically viable to recover US gas than would have been possible with gas prices at $3.00/Mcf.

Mark Lacey said: “More importantly, around two-thirds of the total US gas resource base is in Texas, Pennsylvania, West Virginia and Oklahoma. All of these markets have transportable access to international markets and are conveniently located to export gas to Europe at an attractive price of around $8.90/Mcf.

“This is also likely to boost long-term US gas prices. Rather than retracing back down to their domestic cost of around $3.00/Mcf, we think it makes more sense for prices to trade around $5.00-$6.00/Mcf. Clearly, this increases the attractiveness of US gas companies to investors.”