Small caps favourable once again

Looking at our UK small-cap universe we see a remarkable number of survivors, such as Volex, Johnson Service, Young’s, Gresham House and Sanderson Design. Many of these have naturally had definitive periods to own and disown, Volex being a great recent example. Once a maker of power leads, it has become a world leader in EV charging components in the past five years.

One of our oldest and most consistent veterans is VP group, which came to market in 1973. I often cite this as an early example of a successful family business becoming a very sound long-term plc – as the founding Pilkington family still owns 50%. On flotation, the founder sold £3m of stock to enable the listing. Today, the family stake is worth £200m and the original £3m adjusted for inflation would be worth £38m.

This company has been a consistent dividend payer too, rarely yielding less than 3%. For what it is worth, we think the 2021 valuation of the business is unjustly modest and makes the business vulnerable to a predator if the Pilkingtons were to raise the half-century bat and retire themselves.

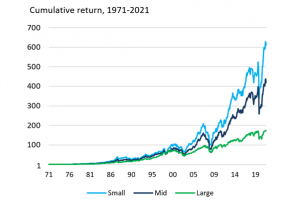

Overall, investing in UK small caps in 1971 against larger caps would have been a very astute move – and that is largely why Tellworth exists. There are a few 1971 things this author craves – Ipswich Town being in the top flight of English football, an original 1971 Mark I Range Rover in Tuscan Blue, and Geoffrey Boycott’s batting average of 100.12. None of these are likely to become 2021 or 2022 realities, but I will keep dreaming while the small caps keep getting bigger.

Long-run returns of size ranked indices, 1971-2021