A new Prime Minister… sustained inflation… long-awaiting interest rate hikes… Japan certainly hasn’t been short on key macro developments in 2024.

And while conventional wisdom suggests equities often drift amid such shifts from the status quo, the county’s leading stock market – the Nikkei 225 – still managed to advance nearly 20% over the year, beating most other indices globally.

We believe this progress sets the stage for another strong period of Japanese equity performance in 2025. Particularly with the nation’s push to improve corporate governance standards continuing to gather momentum.

With this in mind, here are five trends we’ll be keeping an eye on…

1) Shareholder Return Growth

Japan has been reversing its historical reputation for weak shareholder returns for more than a decade now and these returns have been performing strongly in comparison to some other markets over this timeframe. But corporate governance reform entered a new era of urgency in 2023 when the Japan Exchange Group (JPX) began calling for greater focus on corporate value through capital efficiency and management transparency.

The owner of the Tokyo Stock Exchange is urging companies to publicly disclose (in Japanese and English) how they plan to improve their operational and financial returns. The biggest focus is on stocks with a Price to Book Ratio (PBR) of less than 1 – with those companies who are failing to demonstrate how they plan to improve this ratio even being named and shamed.

Source: Morgan Stanley

On the whole, the drive to get companies to do more for investors is working. Disclosures among Prime-listed companies are consistently growing. Likewise, total shareholder payouts are at all-time highs amid record share buybacks and dividends– as the chart above shows.

With the JPX planning to crack down even further, we expect shareholder payouts and disclosures to gather even greater momentum in 2025.

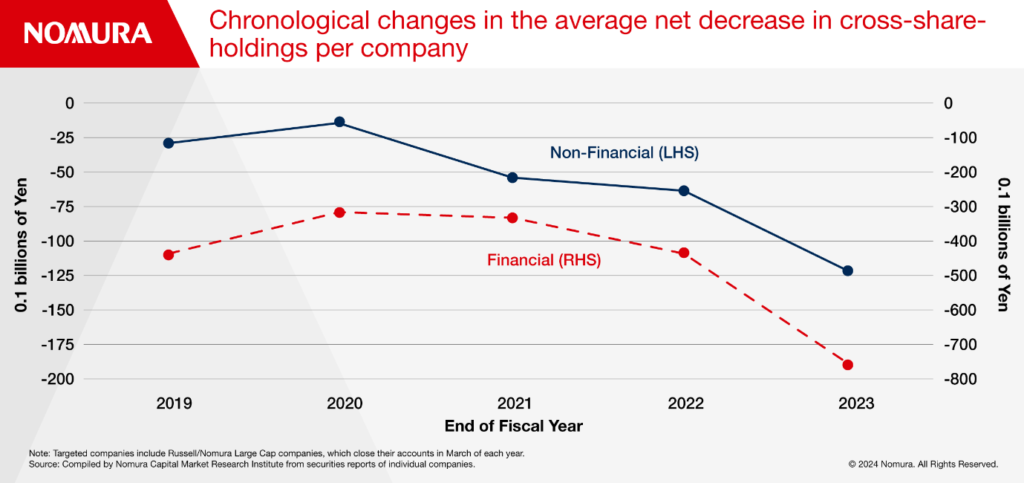

2) Unwinding of Cross-Shareholdings

Cross-shareholding has been a historically popular practice in Japan. The problem with publicly-traded corporations owning stock in one another, though, is a tendency for lower capital efficiency to the detriment of smaller shareholders.

It’s why there has been such a push to unwind them as part of Japan’s corporate governance revolution.

Source: Nomura1

As the chart above shows, there has been progress in recent years. But we feel a real line in the sand was drawn in 2024 as the major casualty insurers, along with some other influential names, committed to liquidating all their cross-shareholdings.

As of the end of May, nearly 70% of the companies listed on the Tokyo Stock Exchange’s Prime market has announced plans to reduce their positions in other companies. As they continue to do so in 2025, it should encourage others to follow suit, free up funds for buybacks, and provide a capital efficiency tailwind to the entire market.

3) Household Cash Reallocation

The savings habits of Japanese citizens are legendary. It’s thought the country’s household cash pile totals some $7.7 trillion – close to the combined GDP of the UK and Germany. But this tendency to hold quite so much wealth in fiat currency finally looks to be changing.

The share of household assets held in stocks and investment trusts hit a record 19.7% at the end of March 2024 and with inflation persisting, equities outperforming, and the yen remaining weak, we expect the shift to continue in 2025. Especially now the Japanese government has significantly expanded its ISA-equivalent tax-free investing plan.

Given the sheer size of Japan’s cash pile, even a small reallocation towards domestic equities could translate into very significant inflows.

4) Possible Return of Foreign Flows

Foreigners bought Japanese stocks aggressively from 2012 to 2016. Since then, however, there has been a pretty consistent year-on-year trend towards selling. In this respect, 2024 was no exception – as the graph below shows.

Source: Morgan Stanley Research; JPX Group

The biggest culprit here is likely the yen. With Japan’s currency continuing to weaken, foreign investors have been reticent to run the risk of losing any gains they make in the conversion process.

The good news is Japan’s stock market performed strongly absent of foreign flows in 2024, emphasising the strength of domestic investment. If the yen was to stabilise and strengthen in 2025, it might prompt a shift back to net foreign buying, providing another tailwind for even stronger equity performance

5) Economic lift from the US

We see two key events playing out in the US next year. One, the Trump administration will take power in January. Two, the economy will continue to strengthen. In our view, both are net positive for Japan.

When the US economy is strong, the global economy tends to be strong. And when you look at the historic performance of Japan, the country has a tendency to follow wider economic trends.

More specifically on Trump, though, Japan enjoys a strong relationship with the US. The nation is unlikely to be hit by any country specific tariff increases the new administration introduces – such as those proposed on Chinese goods.

Meanwhile, if the new president decides to introduce increases charged on all imported goods, we expect Japan’s greatest export to the country – autos – to be somewhat protected by their strong manufacturing presence on US soil.

Richard Aston is portfolio manager of the Chikara Japan Income & Growth Fund and the CC Japan Income & Growth Trust