Inflation is going to surprise investors with quicker-than-expected falls next year, causing investors to rethink their asset allocation, according to Jacob Vijverberg, multi-asset investment manager at Aegon Asset Management.

With inflation having risen sharply due to excess consumer demand, fiscal and monetary stimulus, constrained supply chains and resource security realignment, many investors have feared they will have to adapt to structurally higher inflation. But some of the factors that have caused inflation to rise in the past two years will begin to subside in the coming quarters, says Vijverberg, with ramifications for portfolio positioning.

“Monetary tightening should add downward pressure to consumer prices going forward, with the impact of higher rates increasing mortgage and credit rates as well as consumers’ propensity to save,” he says.

“We also expect less fiscal support for individuals, and the combined effects should cause inflation to fall as consumption of goods and services declines. A slowdown should also eventually cause stickier forms of inflation, like rent and wage inflation, to decline.”

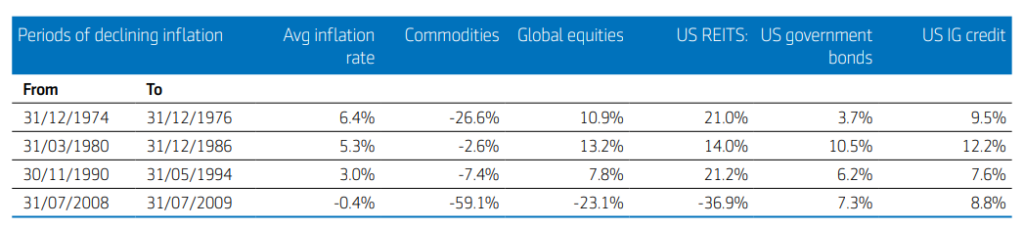

Asset classes that perform well in an inflationary environment are markedly different to those than do well as it comes down, he points out. Looking at key periods of falling inflation[1], different asset classes display a variation of outcomes, which Vijverberg believes makes careful allocation essential for investors at a critical moment such as now.

“The real returns of different asset classes over shorter-term periods of declining inflation show that commodities, which have a high correlation to inflation, decline in value in slowing inflation conditions. However, the causality is unclear. It could be that commodity prices have themselves been the cause of declining inflation.

“The real returns of other asset classes are mainly positive. Falling inflation generally implies a looser monetary policy, which is supportive of risk assets such as equities. In the 2008-2009 period global equities and REITs had sharply negative real returns due to the economic fallout of the Global Financial Crisis.

“The real returns of other asset classes are more mixed. Credit has had negative returns in all falling inflation periods, US REITs have had some positive periods, government debt had one positive period, and global equities two.

While it is difficult to predict the progress of inflation, especially when it becomes self-reinforcing as consumers and business adapt their behaviours in anticipation of higher prices, Vijverberg believes markets are starting to price in inflation falls – making it an important moment for investors to consider their portfolio positioning.

“Markets have begun to price in that inflation will decline, in part due to the action by central banks. High inflation levels cannot be sustained – we expect inflation to fall towards central bank target levels over the medium term.

“Taking such a scenario into consideration, riskier assets such as higher yielding fixed income and equities are likely to outperform lower risk assets such as government bonds. At the same time, we expect commodities to generate a subdued real return.”

[1] Periods of falling inflation include 1974-75, 1980-86, 1990-94 and 2008-09. Source: Bloomberg, Aegon Asset Management (as at August 2022).