2025 was a reminder that Europe still matters (perhaps more than ever), as European equities rallied strongly in 2025. Tom Horsey, Equity Portfolio Manager, Wellington Management, shares his thoughts on European equities.

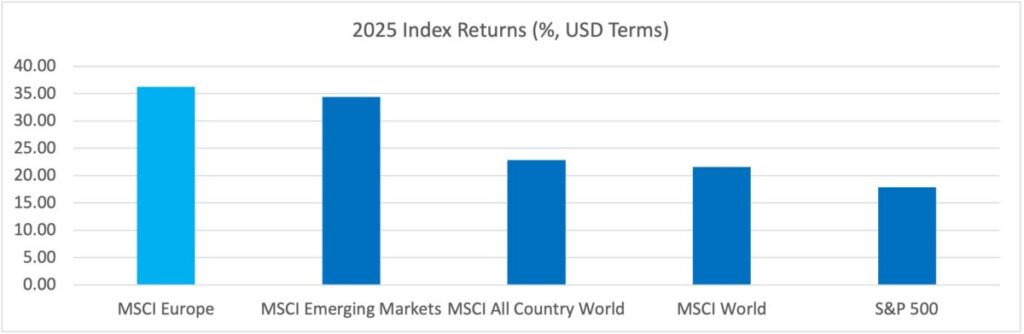

MSCI Europe was one of the best-performing markets in 2025, returning 36.3% in USD terms and outperforming the US (S&P 500), developed markets (MSCI World), emerging markets (MSCI EM) and global indices (MSCI AC World).

More important than the headline return, however, was the shift in market sentiment as investors become less anchored to the familiar knock that “Europe can’t grow” narrative and more willing to underwrite a cycle that is increasingly supported by policy, investments and domestic tailwinds.

The bear case on Europe is well-rehearsed: ageing demographics, chronically low growth, a perceived tech laggard versus the US, and competitive pressure from China in areas like autos and manufacturing. Those challenges haven’t disappeared—but Europe does not need to “beat the US at Big Tech” to deliver strong equity outcomes. The opportunity set is broad (industrials, financials, healthcare, specialised technology, building products, and defence), and many European companies are global in revenue, but European in valuation. Increasingly, we believe European equity deserves to be a standalone allocation for its return potential, diversifying nature and valuation gap relative to the US.

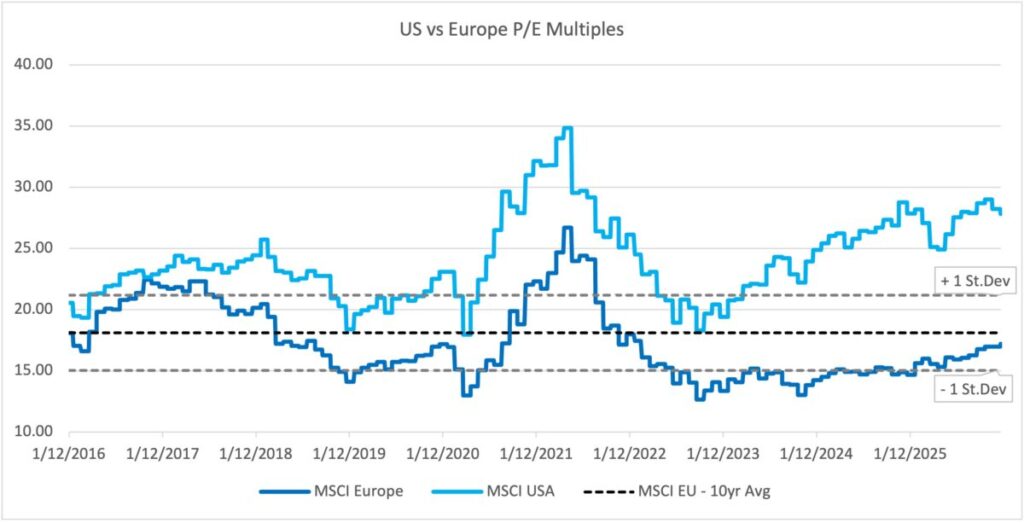

MSCI Europe continues to trade at a meaningful discount to MSCI US (P/E 17.2x vs 27.8x), and below 10Yr average relative to history.

*Source: FactSet, MSCI Dec 2016 to Dec 2025

Setup for 2026: Supportive policy, fiscal impulse and resilient consumers

- Europe is entering 2026 with a more supportive policy mix with the ECB slashing rates in 2025. Moreover, growing share of fiscal spending for many of the European countries is oriented towards security, defence, infrastructure and industrial capacity. This is led by Germany’s effort in aiming to invest EUR 500B across infrastructure, climate and transformation projects over the next decade, which we believe can kickstart and support a more durable multi-year domestic investment cycle.

- Furthermore, we believe European consumers are more resilient and are better positioned than in prior years, with household saving rates inflecting to 15.4% in 2Q25, which is ~2.5% above pre-pandemic level. Real wage growth continues to trend positively alongside stronger household balance sheets, all of which should bode well for consumption in the region.

- One underappreciated feature of Europe today is the number of idiosyncratic “repair and rebuild” stories still playing out across countries and sectors. Greece is a good example of how parts of Europe have structurally improved since the post-2009 financial and sovereign debt crisis. The public balance sheet is stronger, with a larger share of debt locked in at longer maturities and lower funding costs, and the fiscal backdrop has continued to improve as inflation has lifted nominal revenues. The banking system has also undergone a meaningful reset: capital levels are materially higher and non-performing loans have declined toward more normalised European levels. Against this fiscal backdrop, the government has introduced a number of policies heading into 2026—ranging from a 2% cut in income tax rate, to introducing measures designed to support loan growth, to raising defence spending to 3% of GDP—positioning Greece well for a sustained economic up-cycle over the long term.

Areas we are excited about: Defence, Building Materials, Med Tech and Consumer Staples

- In industrials, we believe defence companies continue to remain well positioned for a structural upcycle, driven by increased fiscal spending and geopolitical tensions, making them less sensitive to broader economic cycles. We also think that investors need to think more broadly about domestic infrastructure. Building materials companies that specializes in high performance building materials stand to benefit, as regulatory initiatives, such as EU Renovation Wave and UK Future Homes Standard, and housing shortages spur renewed investment in energy-efficient construction and water systems.

- We are also seeing compelling opportunities in the medical devices and healthcare services industries, supported by durable structural demand drivers such as an ageing population, increased utilisation of diagnostics and lab testing post-COVID. This is translating into sustained demand for age-related solutions such as orthopaedic implants, cardiovascular devices, and home-based monitoring. More importantly, we believe these are structural in nature and end demand are less cyclical in nature with recurring revenue streams through consumables and greater pricing power for providers that offer differentiated services/ medical procedures.

- We see attractive opportunities across a diverse set of European consumer staples businesses as demand strengthens. In food and beverage, healthier eating trends—supported by regulation and shifting consumer preferences—are driving product reformulation toward lower sugar, salt, and saturated fat, and higher fibre content. Food retailing also remains one of the most defensive consumer segments in Europe, underpinned by non-discretionary demand and resilient cash flows. With inflation having pushed consumers toward value formats and private label, discount and convenience channels are well positioned, while ongoing investment in e-commerce and last-mile delivery supports a growing hybrid shopping mode.

The bottom line:

We are constructive on the near-term backdrop for European equities in 2026, supported by accommodative monetary policy, fiscal stimulus, and more resilient consumer demand. We are conscious that global trade tension, tariffs and heightened geopolitics may pose as headwinds for international cyclicals, but we remain positive on domestic-driven sectors such as defence, health care and construction materials.

While we are positive on the immediate outlook for European equities in 2026, our investment philosophy and focus have always been in identifying earnings inflection over the long term. Importantly, many of the companies in the Focused European Equity portfolio today do not require a strong macro environment to outperform, as long as earnings can improve from their cyclical lows. As fundamentals stabilise and sentiment normalises, we see scope for returns to be driven not just by earnings growth but also by selective re-rating.

By Tom Horsey, Equity Portfolio Manager, Wellington Management

For professional, institutional and accredited investors only. While any third-party data used is considered reliable, its accuracy is not guaranteed. Forward-looking statements should not be considered as guarantees or predictions of future events. Past results are not a reliable indicator or future results. This commentary is provided for informational purposes only and should not be viewed as a current or past recommendation and is not intended to constitute investment advice or an offer to sell or the solicitation of an offer to purchase shares or other securities. Holdings vary and there is no guarantee that a portfolio has held or will continue hold any of the securities listed. Wellington assumes no duty to update any information in this material in the event that such information changes .