Inflation-hedging potential

In 2021, the economic recovery and supply-chain disruptions combined to drive inflation higher than central bank targets. Supply shocks brought on by Russia’s invasion of Ukraine accelerated the rise of inflation. In the EU, consumer prices increased by a record 7.5% in March, driven mainly by energy, food and wages.

To combat inflation, central banks including the Bank of England and the Federal Reserve have begun to raise interest rates. The ECB is likely to follow suit, although at a somewhat slower pace than the U.K. and the U.S., given Europe’s exposure to the crisis.

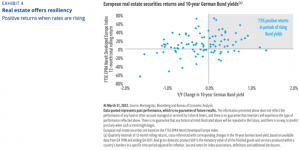

Importantly, European real estate securities have proven to be resilient in periods of rising interest rates (Exhibit 4).

Even as central banks raise rates, we believe inflation is likely to remain higher than it was over the last economic cycle, and that the risk of stagflation is increasing as the war takes a toll on the economy.

Potential inflation buffer

Listed real estate has distinct characteristics that can provide a buffer to inflation. For example, sectors with shorter lease durations—such as self storage—have the ability to reset rents promptly as conditions change. In case of slow growth—or even recession—longer inflation-linked rental contracts offer relatively strong and steady income growth potential.

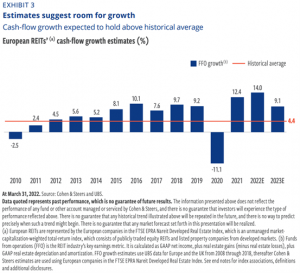

Most commercial leases in Europe explicitly tie rent increases to a published inflation rate. When inflation is extremely high, commercial landlords can increase rental growth income from new tenants and also help them negotiate new and improved lease agreements with existing tenants. Better lease contracts can have a positive effect on investment values, even when interest rates are rising. We believe this characteristic is potentially a strong positive factor for rental and cash-flow growth for European real estate companies in 2022 and 2023.

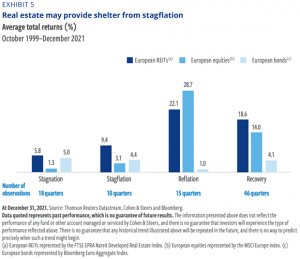

Listed real estate securities may also provide a potentially sturdy backdrop if the economy tips into stagflation, with economic growth slowing while inflation remains elevated. Historically, European REITs have performed well relative to stocks and bonds in stagflationary periods (Exhibit 5).

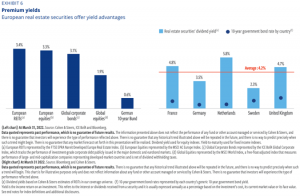

Potential to provide attractive levels of income and growth

European real estate securities also offer attractive yields (with growth potential) relative to traditional asset classes. In addition, they have historically paid high dividends, resulting from their cash-flow-oriented business models and tax-advantaged distributions. Across Europe, real estate securities currently offer meaningful premiums relative to long-term government bond yields, which we believe is an indication of potential value (Exhibit 6).