Economic measures are rarely a major source of controversy. When disagreements over economic measures do arise, however, it is worth deconstructing the source of differences in measurement and interpretation, particularly when they affect policy.

Of late, differences in interpretation of Japan’s output gap, one measure of slack in the economy, have been the subject of discussion over the optimal timing and degree of monetary policy normalisation, as well as the case for counter-cyclical fiscal stimulus. This is because despite three years of above-target core inflation, alongside rebounds in nominal GDP, corporate sentiment indices, private sector investment and—more recently—nominal wages, some measures of the output gap remain negative. These measures indicate the persistence of excess capacity in the economy.

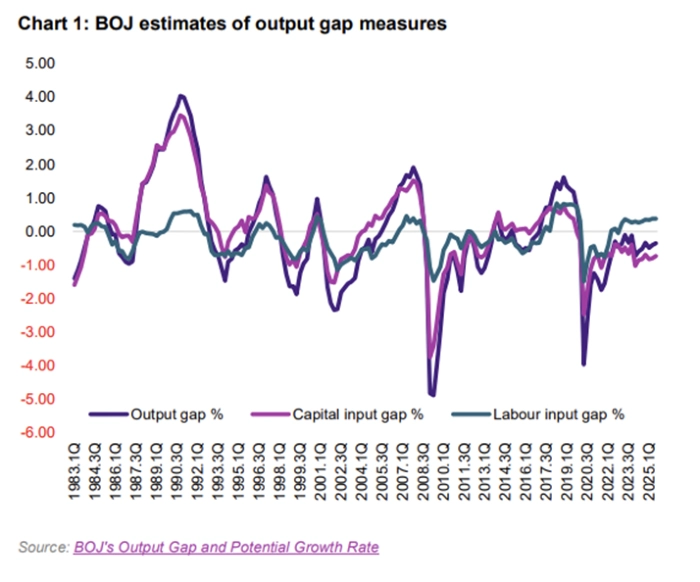

One such measure, released by the Bank of Japan (BOJ), relies on traditional estimation of capital stock and historical shares of output attributable to labour and capital. This approach implies that, due to capital under-utilisation the economy may be producing below its potential output. If this were the principal factor driving prices, inflation would likely be transitory—a pattern that characterised Japan’s “lost decades”.

What is the difference? It’s the labour market

However, a closer look at the BOJ’s own decomposition of the output gap—separating its labour and capital inputs—reveals a more complex story. While capital indeed appears to be under-utilised, labour has remained largely positive, or abovecapacity, since the pandemic. This marks a shift from the conditions during most of Japan’s “lost decades”, which were characterised by capacity under-utilisation.

This shift is subtly reflected in the central bank’s own policy statements, with the BOJ placing greater emphasis on a tighter labour market as a key driver of price expectations, even as the output gap remains a reference indicator. The BOJ appears to be moving away from a simpler “excess capacity” narrative and has been re-evaluating such measures for several years (see, for example, Economic Activity and Prices Outlook, January 2019).

At the same time, the BOJ appears increasingly attentive to investment dynamics and capital renewal. This perspective may implicitly reframe the problem away from levels of capital stock toward deviations from a long-run investment equilibrium, which may itself be higher than currently assumed. This matters for several reasons.

In the “lost decades”, idle capital was perceived as a key constraint

During Japan’s lost decades, including the second Abe administration (2012–2020), weak capital utilisation was perceived as a key constraint to growth and a key reason that nominal growth remained stagnant, with stagnant prices also the norm. Indeed, the labour input gap remained mostly negative between 2012 and early 2017, only turning positive well after capital utilisation began recovering in 2013.

As described above, this is no longer the case. Today, a labour supply shortage—often described as “chronic” by the BOJ— persists even despite signals of under-utilisation of the capital stock.

More broadly, the effectiveness of capital under-utilisation measures depends on how the effective capital stock is defined. There are several reasons why this stock may be mismeasured.

- Legacy capital and the overstatement of effective capacity

The relative dynamics of capital formation and consumption over the “lost decades” indicate that capital renewal slowed and capital stock may have been retained beyond its useful life. This was part and parcel of the deflationary mindset that led to stagnation in private investment. If such assets are still counted as usable capital stock today, they may fail to reflect the true constraints binding firms’ future investment intentions.

- In a tech boom, depreciation schedules may shift rapidly

In the current environment of rapid technological change, capital stock may look large on paper, while being functionally scarce. When technological advancement is driving competition, the need to adopt digitalisation, AI-enabled processes and energy transition requirements may make existing capital obsolete more quickly than during periods when technological innovation is slower. Capital becomes outdated before its original depreciation schedule; as a result, replacement investment may be required even in low-growth economies.

- A higher capital/labour ratio: factor endogeneity

Technological change and the labour market are deeply intertwined. Automation and labour-saving technology are not simply optional productivity upgrades—they are rational responses to labour scarcity. This creates endogeneity between demographics and capital deepening. With fewer workers, there is a higher optimal level of capital per worker, and therefore higher investment demand. This relationship may be missed by traditional measures of the output gap.

Conclusion: wage-price dynamics, not the output gap, are key to future rate policy

Taken together, these considerations suggest that traditional measures of capacity should be treated as only one element within a more diversified BOJ monetary policy toolkit. Even in an environment of low potential growth, resilient capex can coexist with a tight labour market—particularly if the ageing of capital stock has accelerated.

By Naomi Fink, Chief Global Strategist, Amova Asset Management