For decades, investing in emerging markets (EMs) followed a predictable playbook: track local politics and economies, commodity cycles and identify companies with the potential to succeed either in global export markets or fast-growing domestic markets. Ladislav Sabo, portfolio manager at J O Hambro Capital Management, shares insights on EMs.

But over the past three years, that playbook has been fundamentally reshaped by the explosive growth in AI semiconductors and the surge in AI-related infrastructure spending.

The US dominates the market of top-performance chip design through companies like Nvidia, AMD, as well as increasingly through in-house chip design by major semiconductor buyers like Google or Amazon, which are developing their own AI accelerators.

On the other hand, emerging markets are home to the vast supply chain that these companies rely on. Regardless of which US company designs the leading-edge chip, it is, with few exceptions, manufactured by TSMC in Taiwan. One exception is Samsung, whose smaller semiconductor foundry business is also based in an emerging market. Another is Intel, which still maintains its own manufacturing capabilities but has increasingly shifted some production orders to TSMC in recent years to remain competitive.

Emerging Asia’s presence is however not limited just to chip manufacturing; it only starts there. Taiwan, Korea and China offer an ecosystem of companies with leadership in the majority of components found in AI servers, from memory, printed circuit boards, cooling, power supply units and other components to final design and assembly of AI servers.

This reliance on AI infrastructure from emerging Asia has transformed sectoral weightings and EM’s growth profile and subsequently return profile. The technology weighting in the MSCI Emerging Markets Index is 36.8%, which is larger than the technology weighting of the S&P 500 at 35%.

EMs are now seeing an earnings boom they haven’t seen in the last 20 years (with the exception of the rapid earnings recovery in 2010 after the 2009 shock, so not a fair comparison) and this earnings growth is translating into returns.

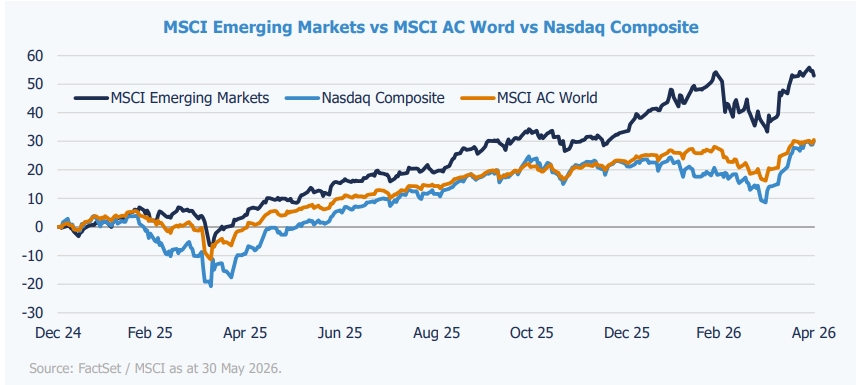

EMs are finally outperforming developed markets after a very long time of lagging returns. Last year, the MSCI EM Index cumulatively returned 52.9%, beating both MSCI AC World at 30.4% and the Nasdaq at 29.9%. The same patterns continue year-to-date.

This outperformance is not simply the result of slightly higher technology weightings, but also of a fundamentally different type of exposure within the technology sector itself.

While both the US market and emerging markets provide exposure to AI, a large share of US technology is concentrated in companies spending heavily on AI, such as Alphabet, Amazon, Meta and Microsoft, where investors have increasingly questioned the returns on these massive investments.

Another large portion of the US technology footprint is in software companies, but these face the risk that rapidly advancing AI capabilities could disrupt their existing business models.

On the other hand, technology companies in emerging markets represent the “picks and shovels” of the AI revolution. While fierce competition to develop leading AI models has weighed on investor enthusiasm for US hyperscalers, the resulting surge in capital expenditure has been a major tailwind for the “picks and shovels” companies in emerging markets that supply the underlying AI infrastructure.

This divergence in AI exposure is likely to become even more pronounced following the eventual IPOs of companies such as OpenAI and Anthropic.

Increasingly, the question of whether emerging markets can outperform the US market may come down to where the greater economic returns from the AI boom ultimately accrue: to the companies spending on AI infrastructure, or to the companies enabling it.

Despite the exceptional performance of emerging markets so far this year, returns have been heavily concentrated. Around 60% of the gains in the MSCI EM Index have been driven by just three stocks: TSMC, Samsung Electronics and SK Hynix.

That said, it would be a mistake to view the EM technology opportunity as being limited to these mega-cap names alone.

Active portfolio managers continue to have access to a broad and diverse opportunity set across the EM technology ecosystem. As discussed earlier, emerging Asia is home to numerous global leaders supplying critical components for AI servers. Many of these companies are well positioned to benefit from rising dollar content as future AI accelerator platforms have and will drive increasingly demanding technology upgrades to support ever-higher computing power requirements.

AI has reshaped how asset allocators should think about emerging markets. Beyond their traditional cyclical characteristics, emerging markets now offer critical and often irreplaceable technology exposure through a deep ecosystem of companies underpinning the AI infrastructure value chain.

While market performance this year has been heavily concentrated in a handful of mega-cap names, it would be a mistake to view EM technology solely through that lens. The large pool of EM companies in the AI supply chain creates a broad and evolving opportunity set for active investment managers, whose ability to identify these structural winners early may leave them better positioned to capitalise on this regime change than passive investment strategies.

We recently covered Emerging Markets in our latest issue of Wealth DFM Magazine, which you can find here!